North River Wealth - 2Q 2025 Market Recap

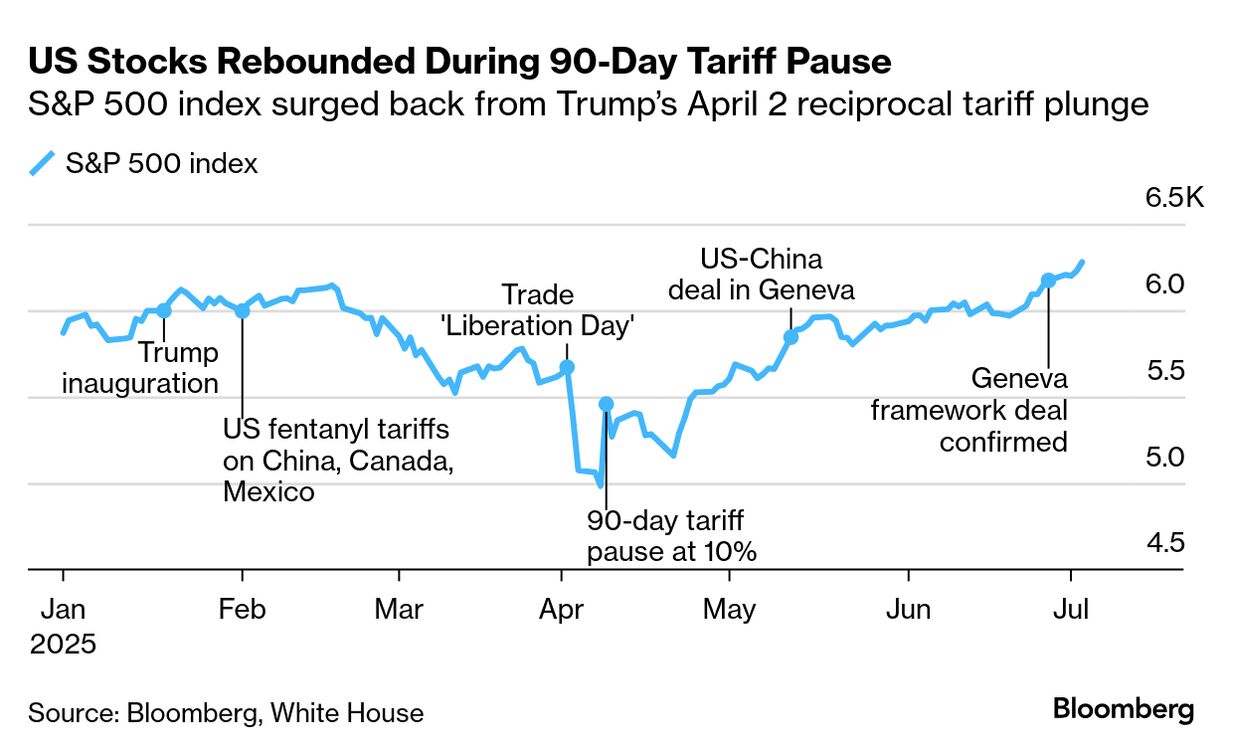

Markets Rebound Sharply After Near 20% Decline

Another quarter, another set of all-time highs in the stock market…just as everyone expected back in April when the S&P 500 was nearly 20% off its peak, right?

After a tariff-driven sell-off in US equities during Q1 and early April that led some investors (though, certainly not our clients 😉) to question market stability, stocks staged a strong comeback in Q2 2025. The rebound was fueled by easing tariffs, cooling inflation, and robust corporate earnings. International and emerging market equities, which had outperformed US stocks in Q1, maintained their momentum into Q2, although the gap narrowed significantly.

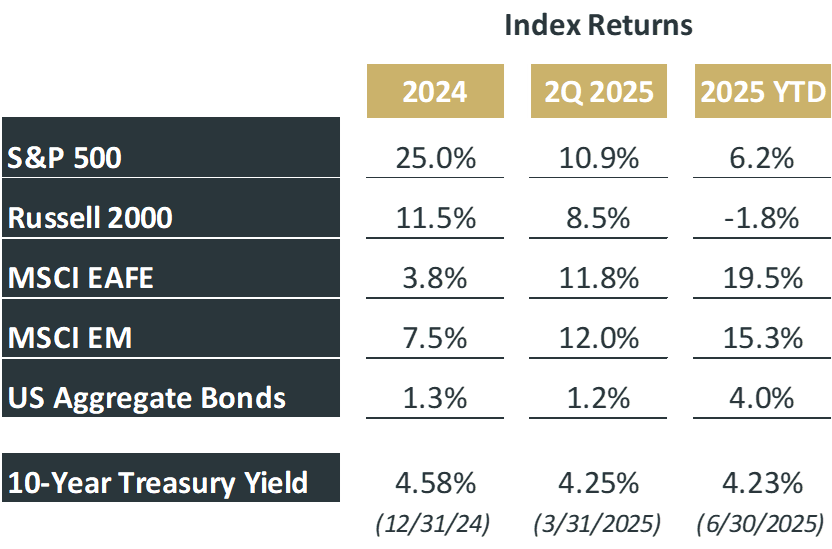

The AI-fueled rally that propelled markets over the past year reasserted itself after a brief pause earlier in 2025. The S&P 500 surged with a double-digit gain for the quarter, bringing its year-to-date return to over 6%. While US small-cap stocks remain down roughly 2% for the year, they posted a solid 8.5% gain for the quarter. Notably, Q2 marked a turning point in AI adoption, as major corporations began deploying generative AI at scale in areas like customer service, software development, and logistics—boosting productivity forecasts and driving increased demand for cloud infrastructure. This shift has not only elevated valuations but also redefined strategic priorities across sectors.

The MSCI EAFE index, which includes stocks from developed countries in Europe and Asia, continued its strong run, benefiting from a weaker dollar. It posted an 11.8% gain for the quarter and is up nearly 20% year-to-date. Meanwhile, emerging markets returned 12% in Q2 and 15% for the year so far.

Interest rates swung wildly throughout the quarter (more on that later), but ultimately the 10-year US Treasury yield saw little change, moving from 4.25% to 4.23%. The U.S. aggregate bond market rose 1% in Q2 and is now up 4% for the year.

Source: BlackRock

The Fed Hints at Potential Rate Cuts

Despite continued pressure from President Trump, the Federal Reserve (an independent government entity), kept interest rates unchanged as the labor market remains strong and inflation appears to be under control. After over a year of “higher for longer” interest rate guidance, softer-than-expected inflation data in April and May gave policymakers some breathing room. As of this writing, markets are still anticipating two rate cuts in 2025, with the first expected as early as Q3. With recession concerns largely behind us, the question for the Fed now isn’t if it should cut rates, but how quickly.

Notably, the Fed’s focus appears to be gradually shifting from inflation to the labor market (the Fed has a dual mandate of price stability and maximum employment). Strong job numbers reduce the urgency for rate cuts and may slow the pace of any policy easing, at least relative to earlier market expectations.

Rate cuts are typically seen as a positive for markets (they can stimulate investment and encourage spending over saving), but they can also signal economic weakness. How the Fed balances these dynamics in the coming months will be a key storyline to watch as the year unfolds.

Bonds: Not That Boring!

Bonds are typically viewed as safe-haven or safer investments relative to stocks, but that is not always the case. As we witnessed during recent inflationary periods, bonds are not always the safest investment to have. They lose purchasing power and offer little projection to rising prices. Despite the President’s desire to bring bond yields lower to help spur more investment, bond yields actually spiked in April before finishing the quarter closer to where they started. Typically, during market sell-offs, bond yields decline (which pushes prices up due to higher demand) as investors move into safer assets. When that didn’t happen this time around, the administration reversed course on some tariff policies, helping to calm the bond market. While not the most dramatic headline of the quarter, it will be worth keeping an eye on supply and demand dynamics in the Treasury market, especially as tariff discussions and trade negotiations continue to evolve.

What's Next: Outlook for Q3 2025

Looking ahead to Q3 and the rest of the year, the anticipated Fed rate cuts may support a soft-landing scenario for the US economy, where inflation continues to fall without triggering a recession. Lower borrowing costs could encourage more consumer spending, business investment, and be a help to the housing market. But, as we know, risks remain including: geopolitical uncertainty, elevated debt levels, and lingering wage pressures.

Still, with monetary policy finally easing and innovation accelerating, the US economy enters the second half of 2025 with cautious optimism. We anticipate continued market strength but with increased selectivity as investors focus on companies demonstrating sustainable competitive advantages and maintaining strong balance sheets in this evolving economic landscape.

Authored by Stephen Blahovec and Michael Rausch of North River Wealth Advisors. We are an independent, fee-only financial planning and investment management firm located in Pittsburgh, PA servicing clients locally and across the country. To learn more, contact us here.

This content is developed by North River Wealth Advisors from sources believed to be providing accurate information. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information and should not be considered a solicitation for the purchase or sale of any security.