North River Wealth - 4Q 2025 Market Recap

Rising unemployment, persistent inflation, tariffs, volatility, the longest government shutdown in U.S. history, concerns on stock market valuations, and yet again, double-digit gains for the U.S. stock market in 2025.

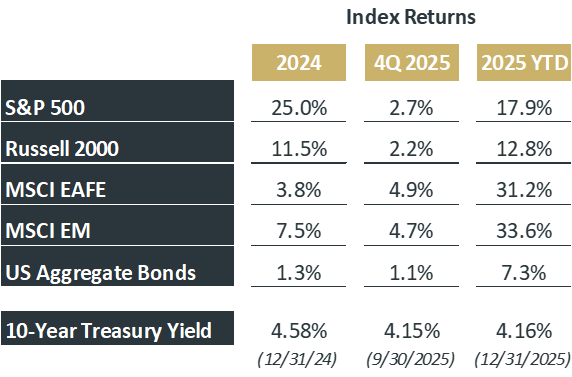

Markets in the fourth quarter continued the momentum seen in Q2 and Q3, with global equity markets (particularly international and emerging market stocks) once again outpacing bond returns. U.S. stocks posted solid gains, with the S&P 500 rising 2.7% for the quarter and finishing the year up nearly 18%. Small-cap stocks also advanced, as the Russell 2000 gained 2.2% in Q4 and ended the year up close to 13%.

Across sectors in 2025, several areas of the market outpaced the broader S&P 500, continuing many familiar themes from years past. Communication Services led the way, with strong returns driven by high growth in media, advertising, and select tech-adjacent names, while Information Technology and Industrials also delivered robust gains. On the flip side, sectors like Consumer Discretionary, Consumer Staples and Real Estate, while posting positive returns, lagged the broader index.

For the first time since 2017, international and emerging market stocks finished as the top two performing equity markets, a notable shift after years of U.S. market leadership. A softer U.S. dollar and relatively attractive valuations abroad helped draw capital toward overseas markets, while certain Asian and European markets saw strong earnings growth. Developed international stocks, measured by the MSCI EAFE Index, climbed 4.9% in the fourth quarter and ended the year up an impressive 31%. Emerging markets continued their strong run as well, gaining 4.7% for the quarter and 34% for the year, driven by a rebound in China’s technology and strength across Latin America.

In fixed income, the Bloomberg Barclays U.S. Aggregate Bond Index advanced 1.1% in the fourth quarter, lifting its year-to-date return to a solid 7.3%. Bond markets found support as inflation data trended lower and investors grew more confident that the Federal Reserve would continue to lower interest rates.

Source: Blackrock

Concentration Concerns in the Resilient U.S. Stock Market

In 2025, market concentration remained a defining characteristic of the S&P 500, with a handful of mega-cap names driving much of the index’s returns. The largest technology and communication services companies — often referred to as the “Magnificent 7” — accounted for an increasingly large share of the index’s total market cap, pushing concentration levels near multi-decade highs. The top 10 largest companies in the S&P 500 made up nearly 41% of the entire index at year end. This imbalance means that index performance can be disproportionately influenced by a small group of stocks, heightening risk if these leaders falter and masking weaker performance among a broader set of companies. Such concentration underscores why diversification within portfolios continues to be an important consideration for long-term investors.

Source: J.P. Morgan Asset Management

The Federal Reserve

The Federal Reserve held two policy meetings during the fourth quarter, accompanied by a steady stream of commentary from Fed officials throughout the period.

At its October meeting, the Federal Open Market Committee (FOMC) lowered interest rates by 0.25%, a move that was broadly anticipated by markets. During his post-meeting press conference, Fed Chair Jerome Powell noted that a follow-up rate cut in December was “not a foregone conclusion,” citing the government shutdown, which limited the availability of current economic data and complicated the policy-setting process.

Despite those concerns, the FOMC proceeded with an additional 0.25% rate cut at its December meeting. Chair Powell emphasized that future rate adjustments would face a higher bar, signaling a more cautious path forward.

Minutes from the December meeting, released on December 30, reinforced the themes outlined in Powell’s press conference. Policymakers expressed ongoing concern about softness in the labor market while remaining attentive to broader economic conditions, including trends among large, consumer-focused companies.

The Federal Reserve’s next meeting is scheduled for January 27–28, marking its first policy gathering of 2026.

2026 Market Outlook

In case you missed our outlook for all things 2026, you can check it out here!

Blessings to you and your family as you start the new year!

Authored by Stephen Blahovec and Michael Rausch of North River Wealth Advisors. We are an independent, fee-only financial planning and investment management firm located in Pittsburgh, PA servicing clients locally and across the country. To learn more, contact us here.

This content is developed by North River Wealth Advisors from sources believed to be providing accurate information. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information and should not be considered a solicitation for the purchase or sale of any security.